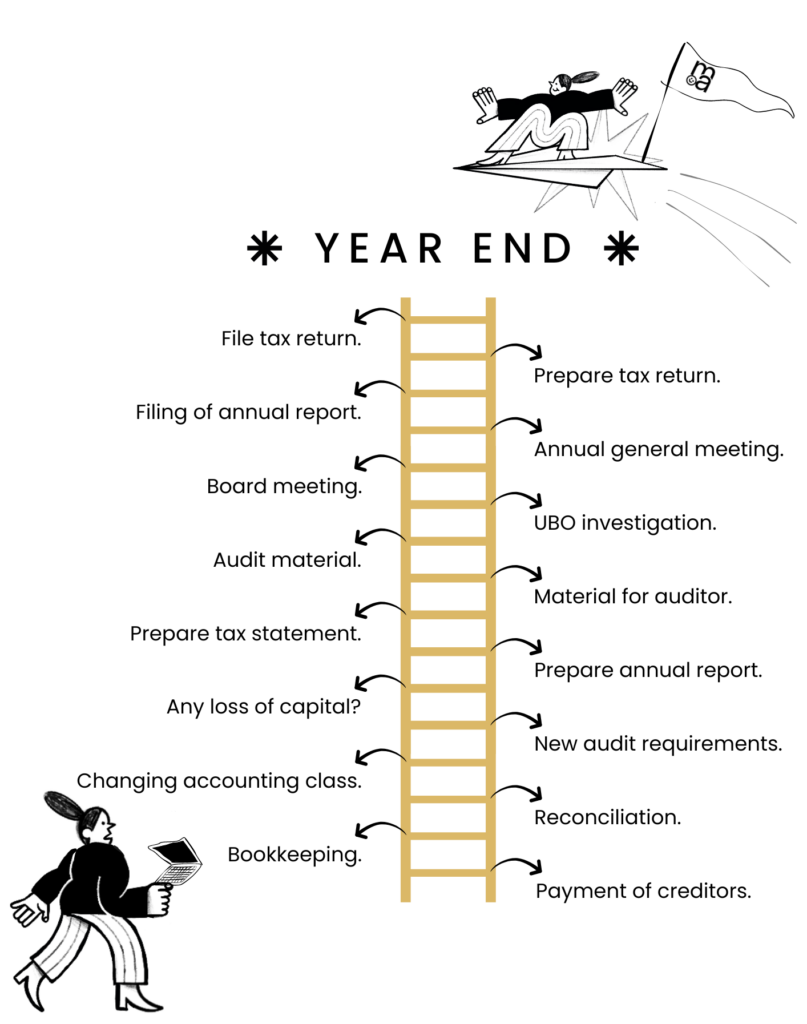

Once the closing of the books is completed, and the final draft of the balance and P&L is prepared, you will now need to prepare the annual report and tax statement.

When doing so, you also need to assess the following:

![]() Are there any changes to the accounting class the company falls within (Regnskabsklasse)?

Are there any changes to the accounting class the company falls within (Regnskabsklasse)?![]() Are there any changes to regulations or audit requirements that you need to take into account?

Are there any changes to regulations or audit requirements that you need to take into account?![]() Has the business experienced any loss of capital or thin capitalization that you need to account for?

Has the business experienced any loss of capital or thin capitalization that you need to account for?

At mighty admins, we can assist you with the entire process from closing the books to the big-picture stuff.

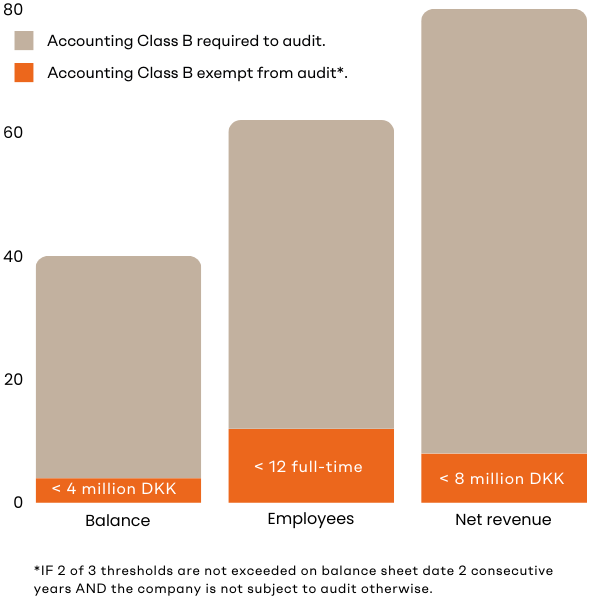

![]() A balance of 4 million DKK.

A balance of 4 million DKK.![]() A net revenue of 8 million DKK.

A net revenue of 8 million DKK.![]() An average of 12 full-time employees during the financial year.

An average of 12 full-time employees during the financial year.

The step after the board meeting approving the annual report is to conduct the annual general meeting. This is where the shareholders of the company are informed about the passing financial year. Here is what must be included on the agenda:

![]() Management must provide a review of the financial year.

Management must provide a review of the financial year.![]() The shareholders must approve the annual report.

The shareholders must approve the annual report.![]() The board is selected and if required, an auditor is elected.

The board is selected and if required, an auditor is elected.

Once the Annual General meeting is over, the annual report must be filed with the Danish Business Authorities – and it must be filed as a special XBRL file.

At mighty admins, we can help you stay compliant with the evolving regulations as well as assist you in facilitating these mandatory steps in the year-end process.

At mighty admins, we can assist you with:

![]() Bookkeeping.

Bookkeeping.![]() Reconciliation.

Reconciliation.![]() Preparation and filing of annual report.

Preparation and filing of annual report.![]() Tax statement.

Tax statement.![]() Preparation of UBO investigation.

Preparation of UBO investigation.![]() UBO documentation.

UBO documentation.![]() Board meeting facilitation and minutes.

Board meeting facilitation and minutes.![]() Preparation and filing of tax return.

Preparation and filing of tax return.![]() Annual general meeting facilitation and minutes.

Annual general meeting facilitation and minutes.![]() … And much more!

… And much more!